Key points:

- Morses Club has delayed its audited accounts

- Is this the Amigo Holdings problem?

- Compensation sclaimis on past loans creating going concern problems?

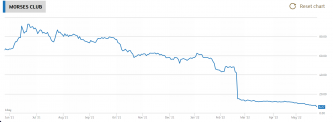

Morses Club (LON: MCL) shares are down again this morning as the company announces that the accounts will be delayed. This just is not a good look for a listed company and that explains the last little tick down on the Morses share price chart:

It's the rest of the decline that needs to be explained more generally. As we've said before about Morses Club the actual operating business seems to be doing fairly well. The problem lies in the historic business. This is what has caused all those problems at Amigo Holdings (LON: AMGO) and which at least partially got resolved yesterday.

If we travel back to late February we can see what's going wrong at Morses Club. But a little background first.

The low credit rating, or high risk, or even “non-traditional” lending market has come under increasing legal pressure in recent years. There have, for a century and more, been varied doorstep lenders and the internet allowed others to arise as well. For whatever reason the powers that be got uncomfortable about such companies. The APR on a loan could be in the hundreds of percent, even as APR is entirely the wrong way to be measuring the costs of small sum and short term lending. Shrieks in The Guardian led to a change in the rules – Wonga went out of business altogether as a result.

Also Read: Should I Buy Stocks During The Current Market Uncertainty?

Amigo and here Morses Club are caught up in this same anti-non-traditional lenders campaign. The rules have changed and so the business model has had to as well. At Morses Club, as we say, the current operating business seems to be doing well enough. Adaptation to the new rules, conformity with them, money being made and so on.

But there's that historic business still to be dealt with. What's been happening is that the compensation lawyers are charging at the company. Possibly business practice didn't change as fast as the rules said it should. Or possibly there are those stretching those changes in the rules. What matters though is that compensation claims are flooding in as a result of the past loan book. It is possible – only possible – that this could eat Morses Club from the inside. Despite the current book looking at least OK, the equity value could end up being passed out to those past borrowers making those compensation claims.

We can't reject that possibility because we've seen it happen before, at least twice (and we can think of a couple of other companies where something similar is happening too).

This latest announcement just adds to the worry. Because why is the audit being delayed? Sure, we're told that the figures would have been here in May, now they'll be by late August. But why?

There's a horrible thought that there might be going concern problems. The auditors need to sign off on the idea that Morses Club has enough capital and good cashflow and so on to be able to continue in business. With the compensation claims flooding in this might be something they're not happy about doing. Which, given other companies in the sector seems a reasonable enough caveat.

Note that we don't know the reason for the delay which means we must speculate. It could in fact be that a reasonable and profitable current business at Morses Club is about to be eaten by those compo claims on the old loan book. We might expect continued volatility as this process is worked through.